Understand Property Taxes and Insurance: What OKC Metro Homeowners Need to Know Before the Monthly Payment Surprises Them

Understand Property Taxes and Insurance: What OKC Metro Homeowners Need to Know Before the Monthly Payment Surprises Them

Property taxes and homeowners insurance are two of the most important parts of owning a home, but they are also two of the most misunderstood.

Most buyers start by thinking about the purchase price.

Then they think about the interest rate.

Then they think about the down payment.

And all of that matters.

But your true monthly payment is not just the price of the house divided into a mortgage. Your monthly payment is usually made up of several pieces, and property taxes and homeowners insurance can make a bigger difference than people expect.

This is especially true in the Oklahoma City metro.

A home in Edmond may have a different tax picture than a similar-priced home in Yukon. A home in Moore may sit in a different county than a home in Mustang. A house in Choctaw, Harrah, Piedmont, Norman, Tuttle, Spencer, or Oklahoma City may carry different property taxes, insurance costs, roof considerations, storm concerns, deductibles, and escrow changes.

Two homes can have the same purchase price and still have very different monthly payments.

That is why I want buyers and homeowners to understand this early, not after closing.

Because surprises are not fun when they show up in your mortgage payment.

Why This Matters So Much

When you buy a home, the lender usually gives you a monthly payment estimate. That estimate may include:

Principal

Interest

Property taxes

Homeowners insurance

Mortgage insurance, if applicable

HOA dues, if applicable

People often hear the payment and think, “Okay, that is my house payment.”

But it is not always fixed forever.

Your principal and interest may stay the same if you have a fixed-rate mortgage, but property taxes and insurance can change. If your taxes increase or your insurance premium goes up, your escrow account may need more money. That can raise your monthly payment even if your interest rate never changes.

This is one of the reasons I talk so much about looking at the whole picture.

A home can be affordable on paper but feel tight later if taxes, insurance, utilities, repairs, and maintenance were not factored in honestly.

You deserve to understand the real monthly cost of owning the home, not just the pretty listing price.

What Property Taxes Actually Pay For

Property taxes help fund local services.

In Oklahoma, property taxes are local. They help pay for things like schools, county services, city services, libraries, technology centers, fire protection, infrastructure, and other local needs.

This is why the tax rate can change depending on exactly where the home is located.

It is not just about the city name.

It is about the county, school district, city or town, technology center district, and other local taxing authorities attached to that specific property.

That is why two homes a few miles apart can have different tax bills.

In the OKC metro, this can matter a lot because many communities cross county or school-district lines.

Edmond can involve Oklahoma County or Logan County depending on the property. Yukon is often associated with Canadian County, but boundaries and school districts can still vary. Moore and Norman are in Cleveland County. Mustang is in Canadian County. Choctaw and Harrah are generally eastern Oklahoma County. Piedmont can involve Canadian County and other nearby county considerations. Tuttle is in Grady County. Spencer is in Oklahoma County.

Those details matter.

Not because one is automatically good or bad, but because they affect the real cost of owning the home.

How Oklahoma Property Taxes Are Generally Figured

Property taxes can feel confusing because there are several steps involved.

Here is the simple version.

A county assessor places a value on the property.

Oklahoma uses an assessed value system, which means the taxable calculation is based on a percentage of fair cash value rather than the full market value. Oklahoma’s assessment structure for real property generally uses a fractional assessment system rather than taxing the full fair cash value directly. Local millage rates are then applied to the taxable value.

Then local millage rates are applied.

A millage rate is basically the tax rate used to calculate property taxes. One mill represents $1 of tax for every $1,000 of taxable assessed value. Local taxing authorities, such as schools, counties, cities, and technology centers, can all be part of the total millage rate.

That is why the millage rate is so important.

A higher millage rate means a higher tax bill, even if the home value is the same.

Why Property Taxes Vary Across the OKC Metro

This is where buyers can get surprised.

They may compare a home in Edmond to a home in Yukon, or a home in Moore to a home in Oklahoma City, and assume that if the price is the same, the payment will be close.

Not always.

Property taxes can vary because of:

County

City limits

School district

Technology center district

Local bond issues

Special assessment areas

Homestead exemption status

Assessed value

Prior ownership changes

New construction status

Oklahoma County’s assessor explains that taxable value is multiplied by the millage rate to calculate taxes due, and Oklahoma County publishes tax rate/millage tables showing different total rates by city, school system, technology center, and county levy.

That means the exact address matters.

Not the general area.

Not the ZIP code alone.

The actual parcel.

That is why I never want buyers to casually assume taxes. I want us looking at the real county record, the current tax amount, the likely future tax picture, and whether the current owner’s exemptions are affecting what we see.

The Homestead Exemption: Do Not Skip This

If you buy a primary residence in Oklahoma, one of the most important things to check after closing is the homestead exemption.

The homestead exemption reduces taxable assessed value for eligible owner-occupied primary residences. Cleveland County explains that the homestead exemption is $1,000 of assessed valuation and may save roughly $75 to $125 depending on the area of the county.

Canadian County explains the same basic $1,000 assessed valuation exemption and notes that savings can vary depending on the local millage levy.

Oklahoma County has noted that homestead exemption can provide property tax savings in the general range of about $75 to $130, and that homeowners must file by the county deadline for the savings to apply for the tax year.

This is not usually a huge monthly amount, but it is still your money.

And more importantly, it is one of those homeowner steps that can be easy to forget in the busyness after closing.

You move.

You unpack.

You change utilities.

You find the silverware.

You try to remember which box has the school papers.

And then property tax paperwork can fall through the cracks.

Do not let it.

After closing, check with your county assessor and file your homestead exemption if the home is your primary residence and you qualify.

Homestead Tips for OKC Metro Buyers

Here are a few practical tips:

File with the county where the property is located.

Do not assume the title company, lender, or REALTOR® files it for you.

Keep proof that you filed.

Ask the county assessor about deadlines.

If the deed changes later because of divorce, death, trust changes, adding or removing someone, or other ownership changes, ask whether you need to reapply.

Canadian County specifically notes that if your deed changes for reasons such as divorce, sale, change of owner, court action, or death of a spouse, you must renew your homestead by March 15.

That is the kind of little detail people do not always know until it matters.

Senior Valuation Freeze and Other Exemptions

Some Oklahoma homeowners may qualify for additional property tax relief programs, such as a senior valuation freeze, depending on age, income, homestead status, and county rules.

Canadian County explains that the senior property valuation freeze applies only to homestead property used as the homeowner’s primary residence and cannot be applied to non-homestead property.

Oklahoma County has also discussed senior valuation freeze eligibility in its assessor information, including income limits and filing deadlines.

If you are helping aging parents downsize, transition, or stay in their home longer, this is something worth asking about.

Do not guess.

Call the county assessor.

Ask what exemptions may apply.

Ask what documents are needed.

Ask when the deadline is.

A ten-minute phone call can save money and stress.

Why New Construction Taxes Can Surprise Buyers

New construction can be exciting.

Fresh finishes.

New layout.

Builder warranties.

Energy efficiency.

Modern floor plans.

Buyers need to understand that the property tax shown online may not always reflect the completed home.

Sometimes the tax record may still show vacant land, a partially completed structure, or a previous valuation. Once the home is fully assessed, the property tax amount may change.

That means the estimated escrow payment at closing may not be the final long-term tax reality.

This can surprise buyers in growth areas like Mustang, Yukon, Piedmont, Edmond, Deer Creek-area neighborhoods, Moore, Norman, and other parts of the metro where new construction has been active.

The practical tip is simple:

Ask what the taxes are based on.

Is the current tax amount based on land only?

Has the completed structure been fully assessed?

Is the lender using an estimate?

What might the tax bill look like once the home is fully valued?

It is better to estimate conservatively than to be shocked later.

Most homeowners with a mortgage pay property taxes and homeowners insurance through escrow.

Escrow means your lender collects money each month as part of your mortgage payment, holds it in an escrow account, and then pays your tax bill and insurance premium when due.

This can be helpful because you are not trying to come up with a large tax or insurance bill all at once.

But escrow is also where payment changes often show up.

If your insurance premium increases or your property taxes rise, the lender may determine that your escrow account is short. When that happens, your monthly payment may increase to cover the new projected amount and sometimes to make up the shortage.

This is one of the most common moments homeowners feel blindsided.

They think, “I have a fixed-rate mortgage. Why did my payment change?”

Usually, it is because the escrow portion changed.

Principal and interest may be fixed.

Taxes and insurance are not always fixed.

How to Read Your Mortgage Payment

When you look at your mortgage statement, try to understand each part.

Principal is the amount going toward paying down the loan balance.

Interest is the cost of borrowing the money.

Escrow is the portion collected for taxes and insurance.

Mortgage insurance may apply if your loan requires it.

Fees or other charges may appear depending on your loan or servicer.

Do not just look at the total.

Learn the pieces.

That way, if the payment changes, you can identify why.

Was it taxes?

Insurance?

Escrow shortage?

Mortgage insurance?

A servicer error?

A new assessment?

A policy renewal?

When you understand the pieces, you feel less helpless.

Homeowners Insurance: What It Is Supposed to Do

Homeowners insurance is designed to help protect you financially if covered damage happens to your home or belongings, or if certain liability situations arise.

A standard homeowners policy often includes coverage categories such as:

Dwelling coverage

Other structures

Personal property

Loss of use/additional living expenses

Personal liability

Medical payments to others

But the details matter.

Not every policy is the same.

Not every type of damage is covered.

Not every roof is covered the same way.

Not every deductible works the same way.

Not every claim is worth filing.

And in Oklahoma, storm risk makes insurance especially important.

Why Oklahoma Homeowners Insurance Deserves Extra Attention

Oklahoma homeowners have to think seriously about wind, hail, tornadoes, roof condition, deductible structure, and storm claims.

The Oklahoma Insurance Department says most standard homeowners policies cover hail damage to roofs and other parts of the home, but policies may include restrictions, such as cosmetic-damage limitations or higher deductibles specifically for hail.

That sentence matters.

Because a buyer may hear “homeowners insurance covers hail” and think they are fully protected in the way they imagine.

But the policy details may tell a more specific story.

You need to know:

Is the roof covered at replacement cost or actual cash value?

Is there a separate wind/hail deductible?

Is the deductible a flat amount or a percentage?

Are there cosmetic damage exclusions?

Are older roofs treated differently?

Are there limitations based on roof age or material?

Is the policy written for replacement cost on the dwelling?

What are the exclusions?

What is the claims process?

These are not tiny details.

These are the details that matter after a storm.

Replacement Cost vs. Actual Cash Value

This is one of the most important insurance concepts for homeowners to understand.

Replacement cost generally means the policy is designed to pay the cost to repair or replace covered property without deducting for depreciation, subject to policy terms and limits.

Actual cash value generally means depreciation is considered.

For roofs, this can be a big deal.

If your roof is older and your policy only covers actual cash value, you may receive much less than you expected after a covered loss because the age and condition of the roof may reduce the payout.

This does not mean every actual cash value policy is wrong.

It means you need to understand what you have.

Especially in Oklahoma.

Roof coverage is not something to skim past.

Wind and Hail Deductibles

Many Oklahoma homeowners have a separate wind and hail deductible.

Sometimes it is a flat amount.

Sometimes it is a percentage.

A percentage deductible can be confusing because it may be based on the dwelling coverage amount, not the amount of damage.

For example, if your dwelling coverage is $300,000 and your wind/hail deductible is 1%, your deductible could be $3,000.

If it is 2%, that could be $6,000.

That is why I always want homeowners to look at their declarations page and ask their insurance agent to explain the deductible in plain language.

Not insurance language.

Real life language.

“If a hailstorm damages my roof, how much would I likely pay out of pocket before insurance starts paying?”

That is the question.

Do Not Choose Insurance Based Only on the Cheapest Premium

I understand wanting the lower payment.

Everyone is trying to make the monthly numbers work.

But the cheapest insurance premium is not always the best protection.

Sometimes a lower premium comes with a higher deductible, weaker roof coverage, exclusions, lower limits, or less protection than you expected.

The goal is not to overpay.

The goal is to understand the tradeoff.

A policy with a higher premium but stronger coverage may be better for one homeowner.

A policy with a higher deductible and lower premium may work for someone with strong savings.

A first-time buyer with limited reserves may need to think carefully before choosing a deductible they could not realistically afford after a storm.

Insurance should fit your risk tolerance, budget, and home.

Not just your desire to lower the monthly payment.

Roof Age Can Affect Insurance

In Oklahoma, roof age matters.

A newer roof can sometimes help with insurability or premium options, depending on the carrier.

An older roof may raise concerns.

Some insurance companies may limit roof coverage, require inspections, charge more, or decline certain risks depending on age and condition.

If you are buying a home, ask:

How old is the roof?

Are there receipts or permits?

Was it replaced after a storm claim?

What material is it?

Are there multiple layers?

Has it been inspected?

Does the insurance quote assume replacement cost or actual cash value?

Will the insurance company require repairs?

Is the roof insurable as-is?

A roof is one of those things that affects inspection, insurance, appraisal confidence, and future resale.

It is not just a line item.

It is part of the whole picture.

Storm Shelters, Mitigation, and Home Safety

Oklahoma homeowners also think about storm safety differently than buyers in many other states.

Storm shelters, safe rooms, roof quality, garage doors, tree maintenance, drainage, and insurance deductibles all become part of the conversation.

The Oklahoma Insurance Department’s Strengthen Oklahoma Homes program provides grants for residential wind and hail mitigation for eligible owner-occupied, primary-residence single-family homes, funded by Oklahoma’s insurance industry rather than the state general budget.

Programs like this are worth watching because they show the bigger picture: in Oklahoma, storm readiness matters.

Not just emotionally.

Financially.

A better-prepared home may be safer, more resilient, and potentially more attractive to future buyers.

How Property Taxes and Insurance Affect Buying Power

Here is where this becomes very practical for buyers.

Let’s say you are approved for a certain monthly payment.

You find two homes.

Both are listed at $285,000.

Home A has lower taxes and lower insurance.

Home B has higher taxes, higher insurance, and an HOA.

The purchase price is the same, but the monthly payment may not be.

That can affect whether the home fits your budget.

It can also affect your debt-to-income ratio and loan approval.

This is why I never want buyers to fall in love with a price tag alone.

We need to look at:

Estimated taxes.

Estimated insurance.

HOA dues.

Loan type.

Mortgage insurance.

Interest rate.

Down payment.

Closing costs.

Utilities.

Maintenance.

Commute.

Upcoming repairs.

That is the real affordability conversation.

How Property Taxes and Insurance Affect Sellers

Sellers need to understand this too.

Buyers are not only asking, “Can I afford the price?”

They are asking, “Can I afford the monthly payment?”

If your home has higher taxes, an older roof, high insurance costs, an HOA, or condition concerns, buyers may factor that into their offer.

That does not mean you have done anything wrong.

It means buyers are looking at the full cost.

A well-maintained home with clear records can help buyers feel more confident.

If the roof is newer, have documentation.

If the HVAC was serviced, keep receipts.

If you installed a storm shelter, keep details.

If you made insurance-related repairs, keep records.

If you filed permits, keep copies.

Confidence matters when buyers are comparing homes.

Tips to Keep Property Taxes From Surprising You

Here are practical ways to stay ahead of property taxes.

Look up the county record before buying

Do not rely only on a listing estimate.

Check the county assessor and treasurer information.

Confirm whether the current taxes include homestead exemption

If the seller has exemptions you will not qualify for, your taxes may change.

Ask whether the home has been recently reassessed

A recent sale or new construction may affect valuation.

Watch for city and school district boundaries

The city name in the mailing address may not tell the full story.

File homestead exemption after closing

Do not assume it happens automatically.

Open tax notices when they arrive

Do not ignore mail from the county.

Review escrow analysis statements

If your lender sends an escrow analysis, read it.

Budget for increases

Even if taxes are reasonable now, plan for changes.

Tips to Keep Insurance From Surprising You

Insurance deserves the same attention.

Get quotes early

Do not wait until the last minute before closing.

Ask about roof coverage

Replacement cost? Actual cash value? Cosmetic exclusions?

Ask about wind/hail deductible

Flat amount or percentage?

Ask about water damage limitations

Water damage coverage can vary, and flooding is usually separate.

Ask about flood insurance

Even if flood insurance is not lender-required, you may still want to understand the risk.

Review liability limits

Especially if you have a pool, animals, acreage, trampoline, or frequent visitors.

Ask about discounts

Security systems, smoke detectors, new roof, impact-resistant roofing, bundling, claims-free history, or mitigation features may matter depending on the carrier.

Review every renewal

Do not let the policy renew blindly year after year without looking.

Keep a home inventory

Photos and videos can help if you ever have to file a claim.

Keep emergency savings equal to your deductible

At minimum, try to know how you would cover your deductible after a storm.

What Buyers Should Ask Before Making an Offer

Before writing an offer, these are smart questions:

What are the current annual property taxes?

Which county is the home in?

What school district and tax district apply?

Does the current tax amount include homestead or other exemptions?

Is this new construction or recently reassessed?

What might taxes look like after purchase?

How old is the roof?

Are there roof replacement records?

Are there insurance claim records available from the seller?

Would insurance be easy to obtain?

What is the estimated homeowners insurance premium?

What deductible would apply for wind and hail?

Is flood insurance recommended or required?

Are there HOA dues?

Are there special assessments?

What repairs could affect insurance or appraisal?

These questions help protect your budget.

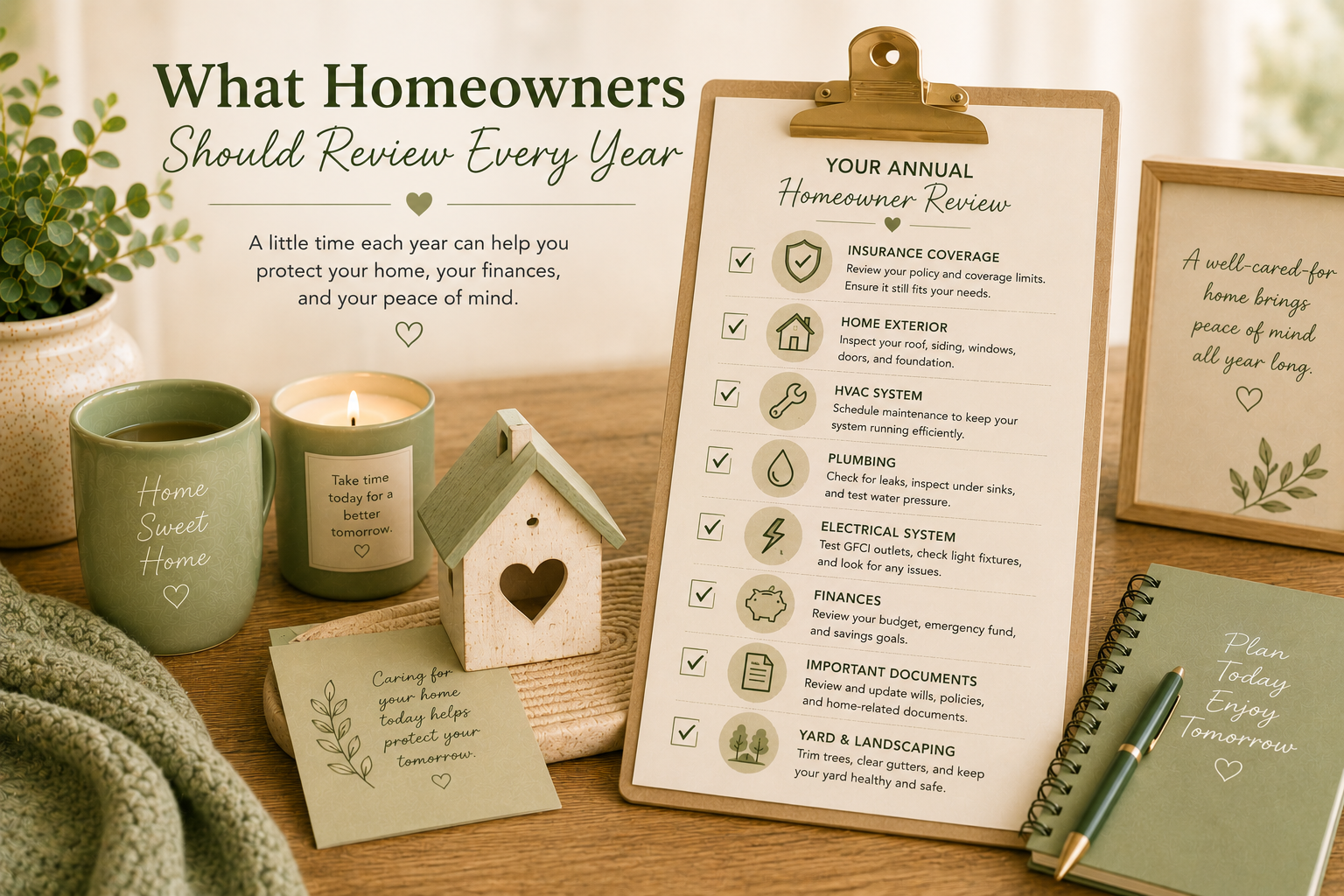

What Homeowners Should Review Every Year

Once you own the home, do a simple annual review.

Property tax review

Check your assessment notice.

Confirm your homestead exemption is still applied if you qualify.

Compare your tax bill to the prior year.

Ask questions if something looks off.

Know your appeal or protest deadlines.

Insurance review

Review your renewal premium.

Check dwelling coverage.

Check roof coverage.

Check deductibles.

Ask about discounts.

Update your home inventory.

Tell your agent about major improvements.

Make sure your coverage still matches your home.

Escrow review

Read your escrow analysis.

Look for shortages.

Look for overages.

Understand whether your payment is changing and why.

This is not exciting paperwork.

But it is powerful paperwork.

It helps you stay in control.

Common Mistakes Buyers and Homeowners Make

Most mistakes happen because nobody explained the details.

Here are some common ones.

Mistake 1: Only comparing purchase prices

A $300,000 home is not automatically the same monthly cost as another $300,000 home.

Taxes and insurance can change the payment.

Mistake 2: Ignoring roof age

In Oklahoma, roof age can affect insurance options, premiums, and future repair risk.

Mistake 3: Not filing homestead exemption

This is a simple savings opportunity for eligible primary residences.

Mistake 4: Choosing the cheapest insurance without understanding coverage

A lower premium may come with a higher deductible or weaker coverage.

Mistake 5: Not budgeting for escrow increases

Taxes and insurance can rise.

Your payment can change.

Mistake 6: Forgetting about new construction reassessment

The first tax amount may not reflect the completed home.

Mistake 7: Not keeping records

Records help with resale, insurance, taxes, and peace of mind.

Mistake 8: Not asking local questions

Online advice from another state may not match Oklahoma taxes, storm risk, insurance, or county processes.

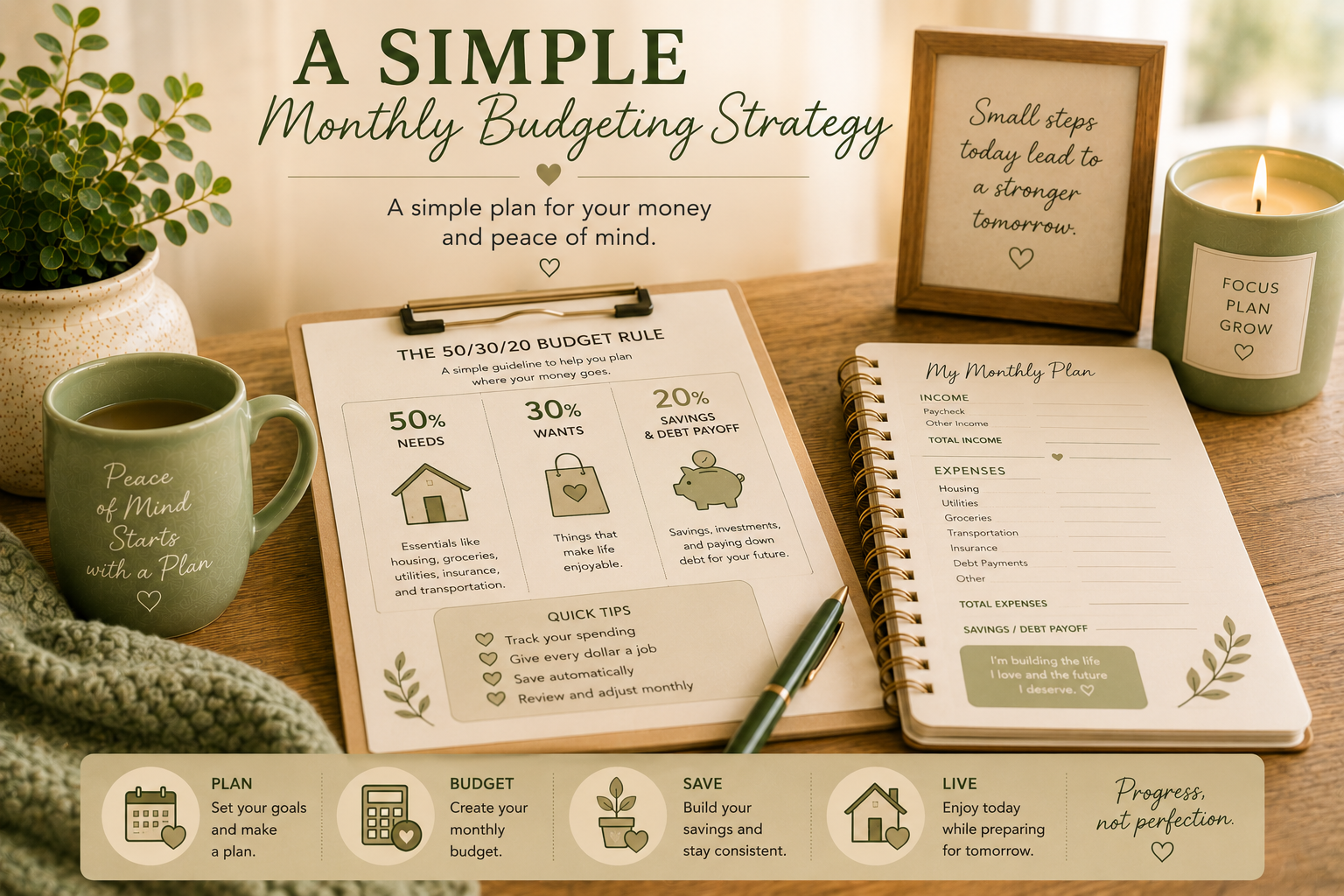

A Simple Monthly Budgeting Strategy

Here is a practical way to think about it.

Start with your mortgage estimate.

Then look at the full monthly picture.

Principal and interest.

Property taxes.

Homeowners insurance.

Mortgage insurance, if applicable.

HOA dues.

Utilities.

Internet.

Trash.

Maintenance savings.

Storm deductible savings.

Repairs.

Lawn care.

Pest control.

For Oklahoma homeowners, I especially like the idea of having a storm-deductible savings goal.

If your wind/hail deductible is $3,000, then that number should not live only on paper. It should be part of your emergency planning.

You may not be able to fund it overnight.

That is okay.

Start small.

Build toward it.

A home emergency fund gives you peace of mind.

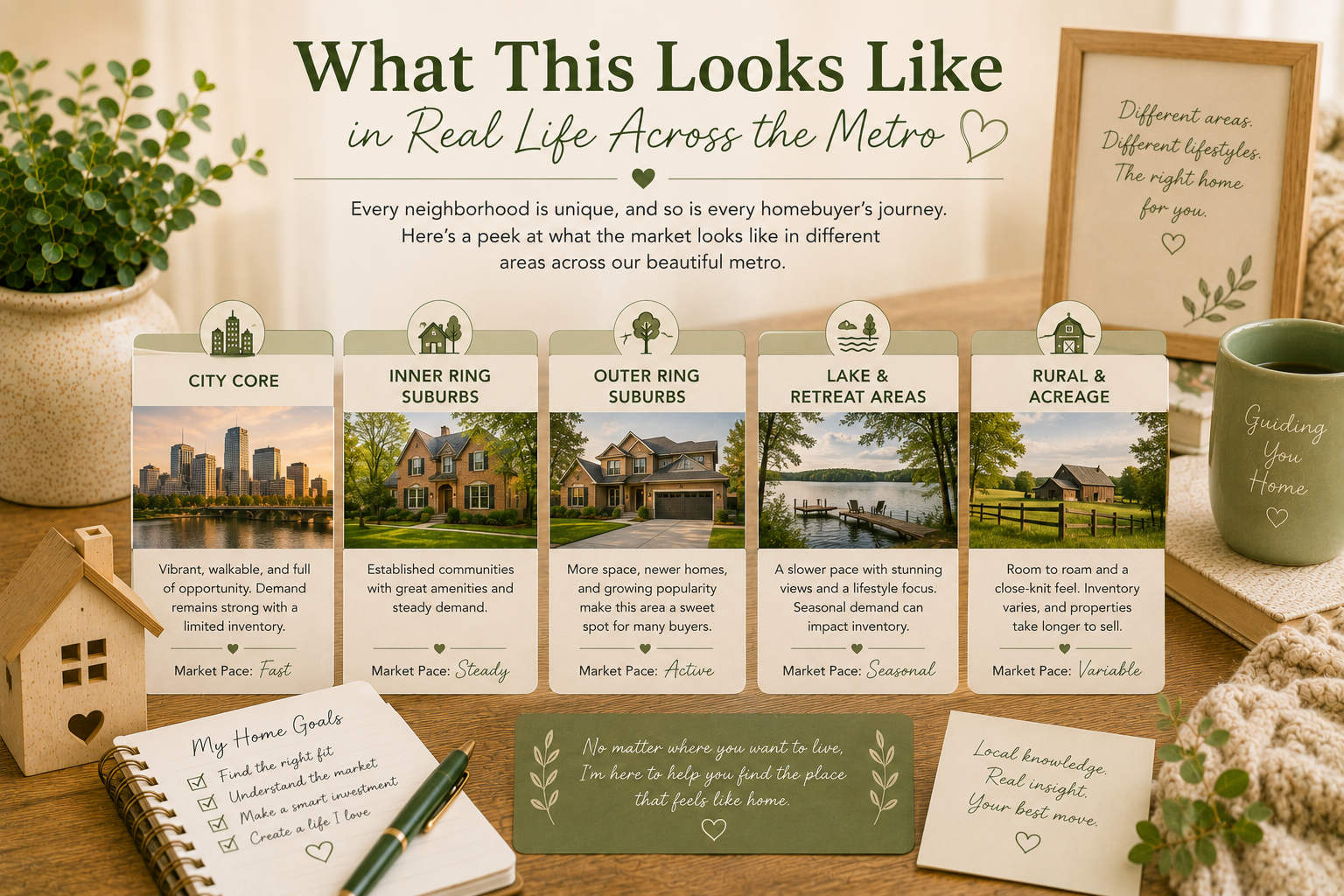

What This Looks Like in Real Life Across the Metro

A buyer looking in Edmond may need to compare not only home prices but county location, school district, taxes, insurance, HOA dues, and roof age.

A buyer looking in Yukon or Mustang may love new construction but needs to ask whether the taxes reflect the completed home.

A buyer looking in Choctaw or Harrah may care about acreage, shops, storm shelters, septic systems, tree coverage, and insurance considerations.

A buyer looking in Moore or Norman may compare older homes, established neighborhoods, school boundaries, roof age, and insurance.

A buyer looking in Spencer or Oklahoma City may focus on affordability but still needs to understand taxes, insurance, condition, and future maintenance.

A seller in any of these areas needs to understand that buyers are calculating the full monthly payment, not just reacting to the list price.

That is why local guidance matters.

My Honest Take

Property taxes and homeowners insurance are not the glamorous part of buying a home.

They are not the pretty kitchen.

They are not the big backyard.

They are not the cozy fireplace or the perfect front porch.

But they matter.

They affect your monthly payment.

They affect your approval.

They affect your budget.

They affect your peace of mind.

They affect whether a home feels like a blessing or a burden six months after closing.

I do not want buyers to be surprised after closing because nobody slowed down to explain escrow, homestead exemption, roof coverage, deductibles, or county tax differences.

I do not want sellers to be caught off guard when buyers ask questions about taxes, roof age, insurance, or monthly affordability.

Real estate is not just about getting to the closing table.

It is about understanding the whole picture.

That is what thoughtful guidance means.

Not pressure.

Not sales talk.

Not “you’ll figure it out later.”

Just honest answers, local context, and a steady guide through the details that actually affect your life.

Insurance Is for Major Losses, Not Minor Maintenance

Homeowners insurance is important. You absolutely want strong coverage, especially in Oklahoma where wind, hail, tornadoes, and roof damage are real concerns.

But insurance should be used carefully.

It is generally meant for major covered losses, not small repairs or routine home maintenance. Many insurance companies report homeowners claims to private claim databases, and claim history can affect future rates, renewals, and whether a company wants to insure the property.

For smaller issues, it is often wise to get repair estimates before filing a claim. If the repair is under your deductible or only slightly above it, filing may not be worth it.

Also, homeowners should be careful when calling their insurance company about possible damage. Depending on the carrier and how the call is handled, even a loss inquiry may create a record. Before sharing details, ask: “Is this just a coverage question, or will this be opened as a claim or reported as a loss inquiry?”

Insurance is there for the big things: tornado damage, major hail damage, fire, significant storm damage, serious water damage, or another major covered event.

It is not a substitute for a home maintenance fund.

The goal is not to avoid insurance when you truly need it. The goal is to use it wisely and protect your future insurability.

Disclaimer

This blog is for general educational purposes only and is not tax, legal, lending, insurance, appraisal, financial, or construction advice. Property taxes, exemptions, assessments, insurance coverage, deductibles, premiums, escrow amounts, claim outcomes, and eligibility for programs or exemptions can vary based on your specific property, county, city, school district, policy, lender, and personal circumstances.

Always verify property tax information directly with the appropriate county assessor or treasurer. Always review insurance questions with a licensed insurance agent. Always discuss loan payment, escrow, and qualification questions with your lender. For tax or legal questions, consult a qualified tax professional or attorney.

As your REALTOR®, my role is to help you ask better questions, understand local real estate context, and connect you with the right professionals so you can make informed decisions.

Thoughtfully, Guiding You Home

If you're navigating buying, selling, or relocating to the OKC metro, I'd love to be your local guide through it, not just the transaction, but the whole picture.

Reach out anytime, no pressure, just honest answers.

405-436-3165

[email protected]

Get Your Free Moving to Oklahoma Guide:

https://susanatlime.com/moving-to-oklahoma-relocation-guide

Get Your Free Listing Launch System:

https://susanatlime.com/seller/launch/system

Get Your Free Buyer Roadmap:

https://susanatlime.com/home-buying-roadmap

Susan Honaker, REALTOR® | Lime Realty

Serving Edmond, OKC, Choctaw, Moore, Yukon, Mustang & the greater OKC metro.

Susan At Lime